|

||||

| Web Sites, Documents and Articles >> Hartford Courant News Articles > | ||

|

Thousands To Feel Mortgage Pain By WILLIAM HATHAWAY, Courant Staff Writer September 10, 2007

Related Links

Homes At Risk

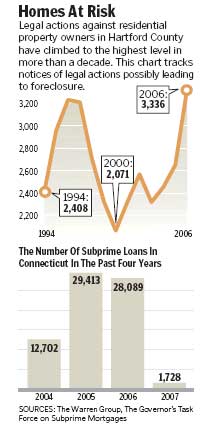

GRAPHIC Dawn Fuller-Ball bought her South End condo in March and she's already in trouble. Despite holding down two jobs, Fuller-Ball is having a hard time paying her bills. Her mortgage broker had told her that despite blemishes on her credit record she could get a loan with no down payment. When she didn't have enough in her savings to qualify for a mortgage, the broker told her not to worry - she could just borrow some from her family, put it temporarily in her account and pay it back after the closing. "I only qualified by the skin of my teeth," Fuller-Ball said. What the 41-year-old first-time homebuyer says she did not fully understand is that she qualified for the loan only because other liabilities as tuition bills, car payments or condo fees were not included when her loan was put together. Fuller-Ball was sold a subprime mortgage - one that does not meet traditional underwriting standards. Community activists say many of them are predatory loans, made by fee-seeking sharks who either lied about conditions of the loan or did not care whether borrowers understood what they meant or whether they could ever pay them back. "It is kind of a scary thing. We are seeing people who haven't had a mortgage for a year and they are already in trouble. Who gave them a loan?" asked Susan Harkett-Turley, executive director of the Housing Education Resource Center in Hartford. Packaged and sold to investors by mortgage brokers, subprime loans are going into default at a rapid pace and causing havoc in financial markets in the United States and around the globe. In Connecticut, where thousands of variable-rate subprime loans are scheduled to jump to higher interest rates in coming months, the anticipated defaults will disrupt local housing markets for the next few years, experts say. In areas with a large number of subprime loans, the higher foreclosure rates will depress housing values and ruin the credit rating and financial dreams of thousands of Connecticut residents. Those expected to be hit the hardest are the working poor and minority residents living in urban areas such as Hartford, where legal actions against residential homeowners - commonly the prelude to foreclosure - doubled in the second quarter of 2007 over the second quarter of 2006. "This could wipe out a whole generation of homeownership opportunities," said Bob Kantor, lead director of the New England community development division of Fannie Mae. Many other areas of the nation have already experienced high rates of foreclosures. The Midwest, which has struggled with heavy job losses, and states like California and Nevada where the speculative real estate bubble has burst, have been hit substantially harder than Connecticut. However, the state is only now beginning to see the effects of the subprime mortgage bust because the more reckless lending practices took root here later than in many other areas of the country, Kantor said. Until about 15 years ago, about 80 percent of all mortgages in Connecticut were written by mortgage banks, which demanded verification of income, proof of savings, a good credit rating and an appraisal of the home that was at least 5 percent more than the value of the loan. Such "prime" loans were then sold to federally backed security companies like Fannie Mae and Freddie Mac, which sold them to investors. But in the past few years, Kantor said, the mortgage lending landscape in Connecticut totally reversed, with 80 percent of mortgages written by brokers, many of whom did not adhere to stringent lending standards. These brokers sold unregulated subprime loans to private investors who, because of rising housing prices, were not concerned about risks. After all, borrowers could simply refinance the worst of the loans and nobody would lose money. That has all changed. According to data collected by the Connecticut Housing Finance Authority, which has convened a task force to study the problem, about 12,000 subprime loans were originated in Connecticut in 2004. But the number more than doubled in 2005, climbing above 29,000. In 2006 the number was about 28,000. And over the past few years, CHFA says, about one in five of those loans became delinquent within the first year, with the problem expected to worsen. As many as one in three of the subprime loans are scheduled to climb to a higher adjustable rate after two years, meaning hundreds of dollars more in monthly payments for borrowers already struggling to make payments. A majority of the loans were made in poorer areas of Connecticut, and experts say they willdisproportionately hurt minority borrowers, like Robin Garrison of Windsor. In 2005, mounting credit card debt led Garrison to refinance the house she had owned since 1997. Like many borrowers, she was lured by low two-year introductory interest rates. She figured that she could always refinance when her monthly payments went up. But last year a family medical emergency caused her to fall behind on her mortgage payments. After months of squabbling with the lender, she managed to defer payment of the outstanding balance until the end of her loan. But then she discovered that her tardy mortgage payments downgraded her credit score and she was unable to refinance. On Sept. 4, the introductory interest rate expired and she was facing a hike of $200 a month in housing payments. "I may be able to make them, but I am struggling," Garrison said. As lenders tighten up on loan qualifications, borrowers such as Garrison and Fuller-Ball find themselves in a trap: They cannot pay the higher monthly payments and cannot refinance into more favorable loans because of tighter lending standards. And it is damage to their credit that worries experts like Kantor. If homeowners like Garrison and Fuller-Ball lose homes to foreclosure, it will be seven to 10 years before they can restore credit and get another home loan. And with fewer available buyers, housing values will be depressed and homeownership rates decrease further - especially in poorer residential neighborhoods in Hartford that have rebounded in the last decade from the housing depression of the early 1990s, Kantor said. "You are wiping out a generation of equity building that is the fastest way to grow wealth in the middle class," Kantor said. Zina Hill-Malcolm is also on the edge. She bought a two-family house near Trinity College in Hartford and was told by her mortgage broker that she was getting a fixed-rate mortgage. In order for her to qualify on her income, the seller agreed to take out a second mortgage, effectively lowering the amount Hill-Malcolm had to borrow. At the closing, she was told the mortgage was not fixed-rate, as she had been led to believe, but an adjustable-rate loan. "He told me not to worry, I could refinance in a year," she said. As her rate crept up throughout the year, she tried to refinance but learned she would have to pay a penalty equal to six months of mortgage payments. With the seller asking her to pay off the second mortgage, Hill-Malcolm eventually did refinance into another mortgage but with a balloon payment due in two years. Unless her financial circumstances change, she fears, she won't be able to pay. "I don't want to lose my home. I feel like I am been duped," Hill-Malcolm said. "I have bills, a disabled child, this is hard." There are a growing number of plans and programs to try to help homebuyers who bought subprime loans. President Bush, Fannie Mae and Gov. M. Jodi Rell, who has set up a task force, have all been discussing strategies that might slow the rate of foreclosures nationally and in Connecticut. Meanwhile, housing counselors are already struggling to meet growing demand for assistance from homeowners like Hill-Malcolm. At the Housing Education Resource Center in Hartford, Harkett-Turley said that in 2006 only 37 people from Hartford County sought help for mortgage-related assistance from her agency. Recently, staff have been seeing at least one person a day and are becoming overwhelmed with work. The Urban League in Hartford, where Hill-Malcolm sought advice, has suspended its one-on-one counseling program for homeowners because of the skyrocketing demand. Instead, the agency plans to run seminars. "Some people were lied to, pressured or information was withheld," said Marie Fort of the Urban League. "Many people thought they had fixed-rate mortgages but did not. They were not even aware of the type of loan they had." "People are trusting," Fort said. "They get excited and rush through the process. It is very easy to sign your name." Courant staff writer Kenneth R. Gosselin contributed to this story.

|

||

| Last update:

September 25, 2012 |

|

||

{kind=link}

|