|

||||

| Web Sites, Documents and Articles >> Hartford Courant News Articles > | ||

|

Loan Delinquencies Rise Foreclosures Highest In Nearly 10 Years As Legislators Debate Borrower Bailouts By KENNETH R. GOSSELIN, Courant Staff Writer March 07, 2008

Related Links

Loan Delinquencies

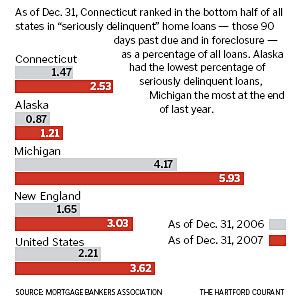

GRAPHIC Home loan delinquencies in Connecticut rose to the highest level since 1985 by the end of last year, with subprime loans accounting for much of the increase. At the same time, mortgage foreclosures climbed to numbers not seen in almost 10 years, according to a quarterly report released Thursday by the Mortgage Bankers Association examining the last three months of 2007. While the figures seem dire, Connecticut was in better shape than many states, ranked in the bottom half in both delinquencies and loans in foreclosure. But the 79 percent increasein "seriously delinquent" loans those 90 days past due and in foreclosure was worse than the nation as a whole compared with a year ago. About 13,000 home loans in Connecticut, or 2.53 percent of all mortgages, were seriously delinquent in the fourth quarter. While that number represents a sliver of the 545,000 mortgages in Connecticut, it could nonetheless have an effect on the larger economy should all the homes go into foreclosure. Housing experts have warned that foreclosures immediately bring down property values in surrounding neighborhoods, sometimes by several thousand dollars. Thursday's report comes as state legislators debate mortgage reform and borrower bailouts. Similar debates are occurring in states across the country and in Congress. Gov. M. Jodi Rell announced a Connecticut housing assistance program primarily for subprime borrowers with adjustable-rate loans who are facing foreclosure. But it was criticized for helping too few, and Democrats subsequently proposed a more aggressive plan to replace it.Housing advocates in the Hartford area say calls from distressed borrowers continue to pour in with no signs of slowing down. "My impression is that things aren't improving," said Andrew Pizor, senior policy counsel at the Connecticut Fair Housing Center. "They are getting worse." Donald L. Klepper-Smith, an economist at DataCore Partners in New Haven, said he believes the housing slump will continue at least through the end of the year and possibly longer. But he said the levels of loan foreclosures in Connecticut, while rising, are not yet at a crisis point. For instance, Thursday's report found that 1.55 percent of home loans in the fourth quarter last year were in foreclosure. Klepper-Smith said he would begin getting more concerned if that number rose to 2 percent or 2.5 percent. "The problem still seems to be relatively contained," he said. Nationally, the number of mortgage delinquencies rose to their highest level in 23 years in the fourth quarter of last year. Connecticut's woes are dwarfed by problems in states such Michigan and Ohio, where seriously delinquent loans represent nearly 6 percent of all loans, the highest in the nation. In Florida, the increase in seriously delinquent loans rose 3.6 percentage points in the fourth quarter, to 5.19 percent, compared with a year ago. The housing downturn was touched off by the subprime mortgage crisis, born of lending some of it blatantly predatory to borrowers who couldn't afford the loans for which they were approved. Most of those were adjustable-rate loans that are now resetting to higher rates, straining household budgets and pushing some borrowers into foreclosure. When home prices were rising, borrowers were building equity and could more easily refinance. That is no longer the case. In the early 1990s, Connecticut saw a wave of delinquencies and foreclosures. But this time things are different. Then, there was a mix of commercial and residential problems. This time around, however, it's almost exclusively residential. Although Connecticut compared favorably with other states at the end of last year, concern is growing about overall mortgage delinquencies, which rose to 5.08 percent of all loans in the last quarter. That compares with 4.29 percent a year ago. "That's higher than I'd like to see it," said Howard Pitkin, the state banking commissioner. Pitkin said he would be more comfortable with 3 percent or lower, which would be a sign of a market regaining stability. Thursday's report also comes at a troubling time for homeowners who have tapped deep into their home equity to meet other expenses. A new report said the average homeowner has less than 50 percent equity for the first time since 1945. Klepper-Smith said there are other pressures on household budgets: The rising cost of food, gasoline and home heating oil. And there is the specter of recession, which could cost the jobs that Connecticut borrowers need to pay their mortgages.

|

||

| Last update:

September 25, 2012 |

|

||

{kind=link}

|